Getting ready to invest? There are some things you should ask yourself

In my first piece about investing for freelancers, I tried to usefully define the process of investing, but how do we go about getting ready to invest? What do we need to do first?

This time I’m going to dive into some of the questions we need to ask ourselves before we can start.

It can be tempting to skip having these conversations with yourself and leap straight into buying investments, but here’s my hot-take on that: don’t.

We need to learn to walk before we can run. And before we can walk we need to check we’ve tied our shoe laces.

There are plenty of stumbling blocks in both creative work and in investing, so this piece is about trying to make sure we don’t trip ourselves up on the way.

Disclaimer: This article is for financial information and education purposes only. It is not financial advice. Investing carries risks. The value of your investments and can go down as well as up and you may not get back the original amount invested. Always do your own research and seek independent advice where required. Read the full disclaimer here.

The great irony of the creative/freelance lifestyle is that despite our deep and (mostly) abiding love of the work, we are in reality, forced to spend more time thinking about financial admin than a typical 9-5 employee. Investing is no exception.

In more traditional roles, employees might benefit from being automatically enrolled in a pension, have the chance to take part in share-purchase schemes and other opportunities. They’ll likely have an HR department to talk them through their options and maybe even perks like life insurance or discounted financial advice.

“Saving is the most effective tool we have for smoothing out that feast and famine cycle and yet it’s often the last thing we’ll actually try”

Sadly, this does not come boxed and ready for freelancers, once we fill in the self-assessment forms. We therefore face a double challenge:

1) We need to learn how to compensate for this lack of a ready-made financial infrastructure by building our own

2) The feast and famine cycle of freelance creative work, as ever, makes it harder for us to predict cashflow and commit to investing

You know the pattern: if you’re in a ‘feast’ stage and loads of work is pouring in, you’re too busy keeping on top of work to spend time sorting pensions or other investments.

However, if you wait for a time when work does go quiet (the ‘famine’ stage), you feel you don’t have the spare cash required to invest, or if you do, that you’re not willing to lock it up for a long period.

So how do we get ourselves in a position to clear these hurdles?

Before we can invest, we need to know that we’ve got ourselves covered elsewhere. This means being in a position where, despite our wobbly income, we know we spending less than we earn (on average) and that we have some cash set aside for emergencies.

“If you don’t have the security of an emergency fund, you could be forced to sell an investment at the worst time”

Regular saving is the most effective tool we have for smoothing out that feast and famine cycle and yet it’s often the last thing we’ll actually try (or it was in my case).

Once you establish that habit, though, you can really create some breathing room for yourself, financially. You’ll also find it will then roll nicely into an investment process, too – as the money you are in the habit of funnelling towards paying off debt or building an emergency fund can then be redirected to your investments.

For most of us, we need to be able to answer ‘yes’ to the following questions:

Building this foundation before we invest is super important. Try and invest before you can say yes to all of the above and you tend to get caught out.

For instance, investing for a return of 7% a year (a fairly typical projection of stock market performance) makes little financial sense if we’re still stacking up debt on a 17.9% APR credit card.

An unexpected owl.

Expecting the unexpected

Likewise, if you don’t have the security of an emergency fund, you could be forced to sell an investment to cover an unforeseen expense. The paradox being that there’s always an unforeseen expense.

If this happens at a point when your investment has dipped then would have to sell at the worst time and may get back less than you put in.

This is important stuff for anyone to understand before they invest, but it’s essential for creative workers to grasp this. The tenuous nature of our work and income already leaves us more exposed to these risks than Mr Monthly-Salary, so we must ensure we have our own backs.

These steps are not new. Follow them and you’ll create a solid foundation for investing – and find life is a lot less stressful as a result.

Why are you investing?

Before you pull the trigger on any investment, you need to know why you are investing and what you actually want to do with the money.

“What do you actually need to do what you want to do? How much is enough?”

Of course, one of the most appealing things about money is that it’s pretty flexible – indeed downright immoral – when it comes to what it can be spent on. However, different investment tools and approaches suit different goals.

For instance, the freelancer investing to provide for their retirement will require a different plan to the freelancer investing to boost their income.

They might pick different kinds of investments (shares or property), different ‘wrappers’ (pensions, ISAs etc. – more on this to come) and have different ideas about the risks they are happy to take along the way.

Turn goals into numbers

Knowing why you are investing will help you understand how much you need and when you will need it. The advantage of being in a creative career is that we’re rarely just blindly chasing a paycheque, so take some time to think about the numbers behind your goals. What do you actually need to do what you want to do? How much is enough?

Come to understand this and it will help you to determine your approach to investing, understand when you have met your goals and give you the motivation to stay the course when there are bumps in the road.

Next time, I’m going to take a look at what investments we can buy, how we can buy them and some of the techniques and ideas that can help us to manage the risks of investing.

Creative Money Guides are ‘How-to’s and explainers relating to specific aspects of money management for those working in the creative industries.

Keeping track of your personal finances can be confusing and painful, so let’s try to layout a path that’s easy to follow

The problem with money is that it’s everywhere. It is in your fridge. Your shoes. Your education. The very screen you are reading this on. It is zapping from your smartphone in myriad micro transactions. Amid this endless swirl of decimal points, it’s really easy to lose yourself in the details and miss the bigger picture.

You know the drill: we think nothing of buying lunch at work or university, but don’t start a pension. We stress daily about our fluctuating incomes, but do not set aside cash when it does come in.

We might even spend some time beating ourselves up about this. But none of this is your fault. You are not bad with money. Rather, as a quirk of evolution, the human brain is just not wired to deal with this stuff.

“Everyone has their own priorities in life, but there are some principles that apply no matter who we are”

Our brains are capable of a lot, but at our deepest level of mental programming, we think we are still hunter gatherers. As creative freelancers in 2020, that means we mostly hunt for work and gather sandwiches. We are trained to acquire and quickly consume the things we need because, historically, the things we need have been perishable.

However, the perishable items we need are now easy to acquire. We do not need to down a mammoth before we can make dinner. Money is not something we can directly physically consume and it is usually intangible, meaning our brain’s default position is to file these things away in our bulging ‘stuff to deal with later’ folder.

In order to tread a better path for the longer term, it helps to use a map. Everyone has their own priorities in life, of course, so these maps will vary for us all, particularly as creative workers, but some principles apply no matter who we are. These are what I call (in annoying-but-catchy blog parlance) the five stupidly simple steps to financial freedom.

They are simple ideas, but they have huge pay-offs. Making ourselves conscious of these steps, periodically checking the map and taking some action to progress along the route, stops us from getting lost, or worse, into debt cycles or nasty financial outcomes.

Below, I’ve broken down each step and listed some of the resources you can work through that might help you with each stage.

Take it a step at a time. Bookmark this page and return to as and when you can. I don’t expect anyone to digest it all and fix their problems overnight, so don’t expect that of yourself, either!

Nor is this an exhaustive list (yet!), this page will act as a bit of a hub and I will update it as I get more relevant material on the site.

Want to make sure you never miss a post? Sign up to the Creative Money newsletter!

If you’ve got this far in life without thinking about these steps, again, I get it. We’re all here because we want to make our living from creative work, not sweating over spreadsheets.

The issue is that money problems absolutely will raise their head at some point in your life and if you’re not prepared for them, the outcomes are not good.

The upside to following these steps is huge. The potential downside that comes from ignoring them is far, far greater

At the milder end, you could wind-up forced-out of your industry, missing out on personal and professional opportunities, or ruining your parents’ retirement.

Even if you’re confident that someone will bail you out, how long will that be the case? And how long will you feel comfortable taking that support?

The upside to following these steps is huge. The potential downside that comes from ignoring them is far, far greater.

Most of us would agree that the hour or so a month it will take you to avoid these outcomes feels entirely worth it when you consider it in this context. What’s more, that time will help you to not just avoid that pain, but very likely give you a disproportionate return in terms of improving your longterm happiness.

Identify the causes of your spending – once you know where it’s going, ask yourself what you are trying to achieve with your spending. Can you come up with a trade-off that doesn’t feel like prohibition? The big longterm wins are usually to be found in your accommodation, transport and food costs but you can make a start right away looking at your day-to-day spending.

We often tell ourselves that building savings is a process of rigorous, joyless discipline. However, thinking in those terms is really unhelpful.

Instead, think about how you can make it easy for yourself to do the right thing. For me, I’ve associated a savings habit with some fairly motivating, positive ideas: mainly the freedom to turn down work I don’t like and the desire to comfortably sustain myself in the down times associated with freelance/creative work.

How do I do this?

Just make a start – remember any savings are better than no savings. The main thing is to get used to getting that money out of your current account (where it might easily be spent) and putting it to better use elsewhere. You might find this piece How to start saving (when you don’t think you can) helpful here.

Know why you’re saving – a deep, personal motivation can make a huge difference to your ability to start saving some cash. Some people want an emergency fund (see below), but sometimes reframing it as ‘the freedom fund’, or ‘the f***-off fund’ can really help. This piece from The Billfold lays out a compelling case for having a f***-off fund.

If you’re in high interest debt, redirect the money you’ve started saving towards repayments. Treat this as a priority – and I mean a genuine priority.

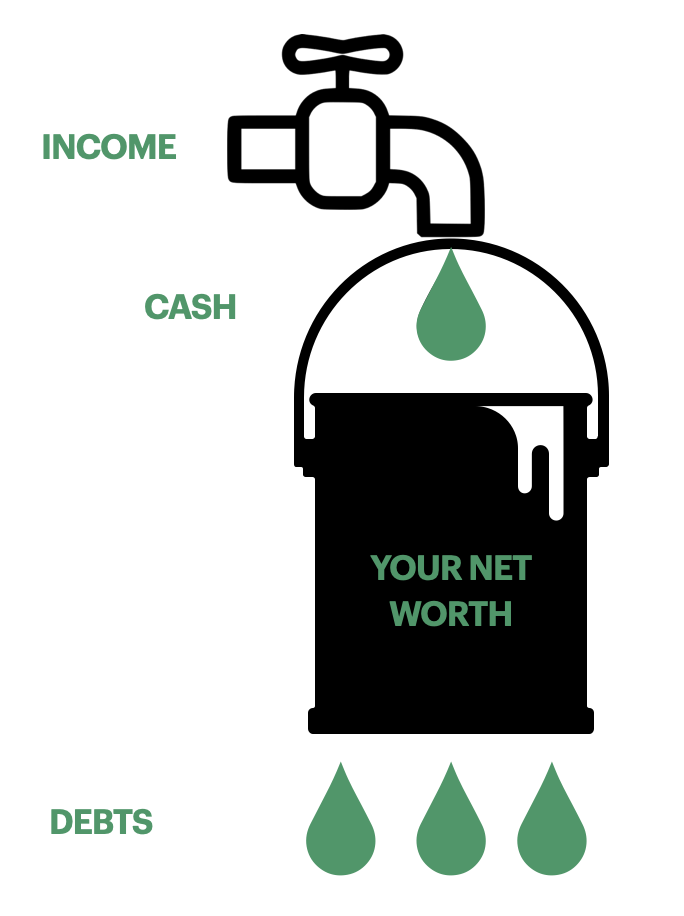

Think about your wealth as water in a bucket. Most of us in creative work have little desire for infinite wealth, but we do want to raise the water level in that bucket to a point where we have a sense of freedom and security.

In this instance, our income is like the tap, sometimes flowing fast, sometimes slowly. However, each debt is a hole in that bucket and if you’re paying interest on those debts, then not only are you losing water, but each of those holes is growing bigger every day. The sooner you act the easier it is plug the holes.

Ignore them, though, and they will grow to the point where the bottom drops out. That looks like bankruptcy, homelessness, relationship breakdown and other things that we very much do not want in our lives.

The excellent US blogger, Mr Money Mustache says you should treat high interest debt as an emergency – as if “your hair is on fire”, so hurl everything you’ve got at it.

How do I do this?

Move high interest debts to lower interest accounts (e.g. a 17.9% interest credit card to a 0% balance transfer card) – this will slow the growth of the debt and mean you can direct more to the actual repayment.

Focus on paying off the highest interest debt – Make minimum payments on the others, when that’s paid off, roll the same payment amount over to the next highest interest debt and so on. This is the time to tighten the belt, maximise that gap between your earnings and spending and funnel everything you can to the debt.

Struggle with motivation? Try Dave Ramsey’s ‘debt snowball’ technique – This approach asks you to order your debts by total owed and pay off the smallest one first, then roll all the payments over to the next smallest and so on. Some people find that clearing those first few small debts is really motivating. One caveat is that it is usually not the best option mathematically, because it can leave you paying more in interest.

Learn to differentiate between good debt and bad debt – not all debts are equal. Taking on a mortgage for the right property might represent a great investment, while racking-up high costs debts on a Buy Now, Pay Later service (Klarna etc.), or putting pints on a credit card, are signs you’re taking on bad debt. These are the ones to jump on ASAP and avoid in the future.

Everyone should have an emergency fund, but if you’re a freelancer or on a variable income (like the majority of creative workers) you absolutely need one.

There is a reason that all good financial advisors and personal finance experts recommend this: you can’t predict what an emergency will look like or when it will come, but it will happen.

Vehicles breakdown. Technology turns on you hours before a show starts. Things get lost or stolen on tour. A work or personal relationship sours suddenly. Houses flood or go on fire. There’s a bloody great pandemic and all work dries up. You get the picture.

How do I do this?

Pick an achievable target – the common advice, and I think it’s solid, is to save £1,000 or a month’s expenses. If things go well with that goal, you can then build that up to three to six months expenses over time.

Keep it somewhere accessible – not in a shoe box, but in a savings account that you can reach with a few hours or at most a few days notice. You will earn horrible interest on it. Accept this.

Do not skip this step – some people think they can do without the emergency fund and move on to the fun ‘make me money’ investment stuff. I have totally tried this approach and am here to tell you it totally does not work out. If the investment drops at the same time as an emergency expense* you are forced to withdraw your money at a point when it’s worth less than you paid-in.

*Finances seem to operate on a ‘Sod’s law’ basis, so if you gamble that it won’t happen, it probably will…

Most people who have built their own wealth have done so via investing or creating businesses. It’s very, very difficult for most of us to simply save our way there.

Investing is the process of buying assets – things that hold some value and can be expected to produce an income (for instance, stocks and shares, which pay a share of a company’s profits, or a property which pays you rental income). In other words: putting the money you save to work making more money.

If you’re not in love with the idea of investing, the trick is to pick something you understand and keep it simple. I have not covered investments on this site yet as I’ve been focussing on some of the previous steps in this list. This will change in the future, but for now here are some key pointers…

How do I do this?

Get going ASAP – the hackneyed phrase in financial circles is that “the best time to invest was 10 years ago, the second best time is today”. This is annoying but also true. As soon as you’ve got debts in hand and some emergency savings, direct that cash to investments.

Start a pension – there is a pensions crisis looming in the creative industries and it’s going to hurt a lot of people. Only 24% of the self-employed save into a pension. The current UK state pension is just £134 a week and likely to fall in real terms over the coming decades. If you don’t have a workplace pension with a company, consider opening a SIPP (Self-Invested Personal Pension). Any amount on top of that state pension is better than no amount. What’s more, even if you’re self-employed, the government will automatically top up your payments by 20% in the form of tax relief, meaning that if you pay in £100 it becomes £120 – and that’s before any return from the investments you put it in. Don’t miss out on that.

Diversify your investments – it’s a very good idea to spread the risk of your investments, so that if things don’t work out then you’re not at the mercy of one market or firm. For this reason, it might be wise to invest in whole markets via low cost index funds (in which you buy a single fund which automatically invests your cash into a small share of every company in the index or stock exchange of your choice). Have a look at Alan Donegan’s guide to index funds. It’s really not hard to get set-up.

Invest for the long-term – if you invest in stocks and shares, think long-term – like 10 years plus. You’re not locking that money away forever and (if you use something like a Stocks & Shares ISA) you can often access it within a few days if need be, but leaving it in there for the long term gives you a far better chance of a decent return. The stock market fluctuates wildly day-to-day, which is why picking individual stocks and so called ‘day trading’ is tantamount to gambling for most. However, it almost always goes up over the long term.

The thinking in this piece has been heavily influenced by a number of financial gurus.

Dave Ramsey we owe for the debt snowball and his renowned concept of the seven ‘Baby steps’, some of which has filtered through here (I don’t agree with it all). Mr Money Mustache continues to influence a lot of my thinking about saving, dealing with debt and investing. Alan and Katie Donegan’s Take Control Of Your Finances course was also really helpful to me in terms of simplifying this overall journey. They were both very generous with their time and humour. They deserve much praise and Mars bars.

The information does not constitute financial advice or recommendation and should not be considered as such. Creative Money is not regulated by the Financial Conduct Authority (FCA), its authors are not financial advisors and are therefore not authorised to offer financial advice.

Investing carries risks – the value of investments and any income derived from them can fall as well as rise and you may not get back the original amount you invested. Always do your own research and seek independent financial advice where required.

From monetising hobbies, to podcasting and pensions – we discuss managing your money as a freelancer

Lily Canter is a freelance personal finance journalist and lecturer (among other things) who writes for this likes of the Metro, The Daily Telegraph, The Guardian, The Times and South China Morning Post.

I first heard of Lily via her excellent Freelancing For Journalists podcasts, which she launched earlier this year with fellow freelancer Emma Wilkinson. As someone who spends much of their days pitching and writing about personal finances, I figured she would have some great insights on the trickier issues facing freelance creatives (hello again irregular cashflow and lack of pension/holiday infrastructure!) I was not disappointed.

We spoke about Lily’s portfolio career, the challenges and merits of her Freelancing For Journalists side hustle and the methods she’s using to funnel a significant slice of her earnings into savings.

Lily Canter… Freelance journalist, lecturer, author, trainer and so on!

How would you describe your role? It’s definitely in the multi-hyphenate territory, right?

“I say I have a ‘portfolio career’! Fundamentally, I’m a journalist, but I’m also a lecturer, a podcaster, trainer, I’m also a running coach and I’m starting to write books as well, but I suppose it comes under the journalism. Then Freelancing For Journalists is part of what I do. I think it’s probably about 10% but that changes depending on what is happening, like when we’re running a training course. Then my teaching is about 30% and my journalism work is about 60%.

“I’m very old fashioned, so I keep track with a diary and when I’m doing something with a person, I highlight it and I tend to work about a month in advance. “

“How do I split my personal and professional finances? I don’t really!”

“We wrote the book first and then got some funding from the university to do the podcast series. It was initially meant to be a learning tool for students and it spun off from that. We had an initial budget for six episodes and we based them on chapters of our book. We had a good three months of planning, we did it in the radio studio, with students helping us to record it and the idea was that it was also work experience for students.

“Then lockdown happened and we still had a few episodes to record, so we ended up shifting to Zoom and doing nine episodes. People liked that first series, so we convinced the university to give us money to buy mics and then we did a second series.”

I like that you found a way to fund it without sinking your own time and money into it. How is it going to in terms of sponsorship or monetising it?

“OK. We’ve had a lot of people who have been positive and we’ve got one sponsor lined-up [for the next series] and we need to decide if we wait for more, or go ahead and see if we pick them up on the way. I’d been warned that would be the case, though, and I’m always thinking of other ways of monetising it. We’ve not gone down the Patreon route as a lot of our listeners are new or starting out and I’m not sure if they can afford it. We have Ko-Fi but it’s just the occasional cup of tea, really! It’s fiddly to use though, you have to go on the site, but we thought we’d try it out. But at the moment it’s more about building the audience and then the training work we’re doing is a by-product of the podcast.”

Want to make sure you never miss a post? Sign up to the Creative Money newsletter!

These projects often lead to things, don’t they? Even if the pay-off isn’t immediately obvious.

“Yeah. We’ve certainly got commissions to write stuff for other platforms about freelancing off the back of it, we can promote the book and it’s certainly a good marketing tool for the Freelancing For Journalists brand. I think it’s what we’re most known for. We’ve been doing guest lectures on freelancing as well. We’ve also run some of our own webinars and that’s been the nice thing about lockdown, people have found their own ways of making money. We did a couple in the summer and they both did well. It was a good way to test the market.”

How do you split your personal and professional finances as a freelancer?

“I don’t really! I still have my personal account. My salary from the university goes into there and my freelance stuff goes into there and then I have a savings account attached. So I have a target of what I want to earn every month and then anything over that is a bonus, then a proportion of that – nearly 50% – I save and that’s in there for tax and pension and anything else. We do have a joint account, too, and my husband and I put money in there as a holiday pot.”

“Previously, I had a full-time job as an academic with a massive pension, so I’m trying to match that and save like eight grand a year.”

That’s interesting – I think a lot of freelancers and self-employed don’t think about regularly setting money aside for holidays and time off like that.

“It was sort of an accident. It was originally a pot to pay off a car, so we were each putting a certain amount away ready to pay it off, then once we did, we didn’t cancel the standing orders. We just carried on on and that became our holiday fund. I used to be really rigid with that stuff when I had a salary. I’m much more flexible now, because my income is much more flexible, but I do check my balance pretty much every day. It’s a bit like my diary, in that I keep track of it all the time. I’m also trying to save quite a lot into my pension. I had a full-time job as an academic with a massive pension [a perk that I lost access to going freelance], so I’m trying to match that and save like eight grand a year.”

That’s a decent savings rate! A lot of freelancers don’t like locking money into a pension because they feel they may need it before pension age. How do you handle that?

“I tend to let it build up over time and then move it over once or twice a year in lump sums. So, for instance, I didn’t get any [SEISS] grants, because last year I earned more from employed work than self-employed. Fortunately, I had some money saved which was [intended to be paid into] my pension pot – so I did need it and I’ve got to build that up again now.

“I have a LISA, which I put four grand a year into [as retirement savings], so I build it up and stick it in there, then I’m still sorting my personal pension with my financial advisor. We’ve got a rainy day fund elsewhere, for the joint account, and I always make sure we have at least £1,000 there as a float, so we overpay into that essentially. Then we’ve got other stuff, like we’ve never touched our child benefit, it just goes straight into savings. The idea is it’s there for when the kids turn 18, but if we suddenly need money to buy a new car, we’ve got it!”

The Freelancing For Journalists podcast covers everything from finances to lifestyle and imposter syndrome.

What else helps you stay on track with savings?

“I look at my bank balance and try to keep a minimum amount in there and then anything over that goes into savings. But I’ve always saved. I’ve barely used credit cards. I’ve never got a car on finance. I just don’t believe in spending if you haven’t got it. Every six months I’ll do a kind of audit just to track if I’m on target with my savings, or earning enough and, if I need to, I look at my spending, or if I can pitch and deliver more work. Even the high street banking apps now tell you what you spend your money on and basically I spend all my money on running: gear, races and a personal trainer. That’s like 90% of my money and the last 10% is probably wine!”

“Well, I also coach a group of runners and I charge them now. I did it for nine months for free and it took up more and more of my time and I’d built up this relationship with them. My view was that I’ll be out running anyway, so why not make an income from it? So I started charging a small amount and I make an income from it. I’ve signed up for some coaching training and warned them all that as soon as I’m qualified, my rates will be going up. There’s tax benefits, too, so quite a lot of the gear that I buy is now tax deductible.”

“My view was that I’ll be out running anyway, so why not make an income from it?”

Have you made any significant mistakes with money?

“I do splash out every now and then. We bought a painting right before lockdown, which we never do and that might not have been the best time to do it! We felt bad about it, which is daft because it’s been years since we’ve done something like that. Then once when I left a job and got a load of holiday money and I went and bought an £800 chair, which no-one ever sits in! So every now and then I do that kind of thing, but only if the money is there.

“There are a couple of things I’ve signed up for this year that I regret. There have been a lot of membership communities and one I signed up for after doing an interview with somebody who really enjoyed it and it was just a total waste of money. It was not what I thought it was going to be. But there are other things that have felt worthwhile.

What has given you good value, do you feel?

“I do subscribe to Journo Resources. We work a lot with Jem and I just really want to support what they’re doing. It’s useful and it’s good for keeping tabs on what’s happening on the freelance journalism world, but it’s more about just supporting what she’s doing. I also know that I can call on her for advice and I don’t feel guilty about it, if I’m subscribing! But I just think everything they do is really good and she’s nailed it, really.”

We do a lot of moaning as freelancers about payments (and, quite rightly, because the system is broken, really). But how would you fix it?

“There’s various things. Transparency about rates is one and that is happening. The #FreelancePayGap list that Anna Codrea-Rado started is really useful. It puts you in a better position to negotiate and allows you to push back when an editor is offering you a certain rate. I guess it’s also educating companies and editors that it’s not just an admin thing. It’s not just ‘Sorry I forgot to pay your invoice’, it’s people’s livelihoods. I’ve never enforced late payments fees, but I do send stroppy emails. I think we just need to be more transparent and not be afraid to talk about money or ask for more money and to be paid. But also, just don’t work for people who don’t pay you properly or pay you on time, in the long run it’s just not worth it, so don’t do it!”

How I Make It Work is a series of interviews with a variety of creative professionals, where we discuss personal experiences and lessons learned about money in the creative industries.