Mallinder’s innovations with Cabaret Voltaire and continuing contribution to electronic music (via the likes of Wrangler and Creep Show) have proven to be hugely influential. He has played all over the world, received great critical acclaim and sold a significant amount of records. He is, by almost every criteria, a very successful musician and yet as you’ll see in the piece, he has nonetheless operated in a huge variety of (mostly enjoyable) roles in order to sustain himself throughout his three decades in the music industry.

Want to make sure you never miss a post? Sign up to the Creative Money newsletter!

For those of us who earn the majority of our living from creative activities, it can be easy to think that engaging with ‘other work’ is a kind of failure. That if you do, you’ve somehow cocked it up – you had it and it got away. Hearing Stephen’s succinct point that “sometimes you have to work” was liberating, in this respect.

Thinking that you’re a ‘creative’ or nothing is, ironically, likely to hasten your permanent exit from a creative industry

Last week, DJ/presenter Shell Zenner discussed how important it is to diversify and to have multiple skillsets. The longer you want to sustain yourself in the creative industries, the more important this becomes. Likewise, it’s perhaps equally important to accept that there will be times when things are off-the-boil with your ‘main’ activity and you might just want, or need, to try something different.

The binary thinking that you’re a ‘creative’ or nothing is, ironically, likely to hasten your permanent exit from a creative industry – either due to the financial pressures of operating solely on the ‘starving artist’ axis, or because doing the same work becomes so unsatisfying that you become disillusioned with the whole thing.

Primary path

Mallinder talks instead about dedication to a ‘primary path’ – from which you will periodically meander and return. He discusses this in terms of making music, but it could be any creative practice that you consider your ‘core’ activity. Our conversation made me realise that the longer you are in an industry, the more likely it is that you will diverge from that primary path and that at some point this becomes not just acceptable, but entirely necessary.

Inspiration and opportunities tend to come in waves – bills do not…

You need to learn new things, to question what you do and push yourself in order to develop your creative practice. Otherwise, it just gets stale. Doing different work, whether developing a new skillset in your existing industry, taking a role outside of it, or doing something like teaching, can therefore be really beneficial not just to your finances, but also to the way you think about your ‘primary path’.

Sometimes you will have to do certain jobs simply to keep the lights on – and they won’t always feel beneficial. Inspiration and opportunities tend to come in waves, after all – bills do not. What matters is understanding that you can, and likely will, come back to that primary path – that there are multiple ways to be creative and to make that your life. Sometimes you will have to ‘work’ then, but that is no failure.

Short Cuts is Creative Money’s series of quick tips, tricks and thoughts about saving or making money in the creative industries.

The electronic music pioneer on how adaptation and determination have proven to be the watch words for his diverse music career

Stephen Mallinder rose to prominence with Cabaret Voltaire in the late 70s, becoming one of Rough Trade’s early signings and establishing an approach to experimental music-making which would prove to be hugely influential in the electronic/ club scene.

In the intervening years, Mallinder remained embedded in music, working in all manner of roles and gaining his doctorate. He has continued to create and innovate and currently works under various monikers, most notably as part of electronic trio Wrangler (with Phil Winter of Tunng-fame and Benge) and Creep Show, with US singer-songwriter John Grant.

What’s more, he also finds time to teach on Brighton University’s Digital Music and Sound Arts degree and masters courses. Mallinder was kind enough to speak to Creative Money about how he has learned to adapt and survive, financially, despite opting for a career in experimental music-making…

How do you feel the way you work with money has helped or hindered your creative journey?

“It’s interesting. I’m part of the Sound Art programme here at Brighton, so I work with students and it is scary. It’s always been scary, how creative people move on from there. It’s alright when you’re at university and you’ve got all these great ideas and you’ve got facilities, but it’s how you function outside there. It’s obviously much more problematic now, too, with what’s happened.

“If you do music, you can’t afford to be mono-cultural in the way you approach it”

“We’ve leapt into so many unknowns in the last 20 years, really since digitisation came along. Originally the arrival of the CD gave us this big splurge, or really, for older artists, the opportunity to re-sell their back catalogue, which worked for labels and that transformed everything, but since then the loss of ‘the product’ and the move to streaming and digital forms has massively affected people. So I think there had to have been an adaptation and I’ve kind of been through all of that.”

How did you first start to adapt?

“My adaptation was really that I realised I needed multiple ways of existing. My daughters were born in the early 90s and at that point, it was like, ‘Wow, this is really difficult…’ We were still making music, we still had our own label, but there wasn’t much [coming in] and it was hard to survive.

“I went to Australia and I lived in Australia for a while. Part of that was needing to find other ways of doing what I do and I ended up doing lots of different things. So I ran a radio station, I ran a record label, I started a production company.”

Want to make sure you never miss a post? Sign up to the Creative Money newsletter!

“I think I quickly adapted to the idea that if you do music, you can’t afford to be mono-cultural in the way you approach it. Or you can, but it’s difficult to go, ‘I make music, I make money out of selling music and doing gigs.’ That’s alright but you’ve got to be smarter with it, really. I ended up working in different parallel ways. I wrote for magazines and newspapers. I did all these things. That kind of prepared me for the world as it has been for the last 20 years, really, this ‘streamed world’. I rapidly became flexible in how I saw it.”

“When I started, you didn’t really do it for money, but then you make money out of it and you feel, ‘Oh well, I do well enough that it owes me a living’. It doesn’t work that way, though, so I think you just have to be flexible. If you want to make music then you just have to be understanding. Your expectations have to be reined in a little bit. Perhaps what I’m saying is that there has to be separation between the creative process and the entrepreneurial, money-making process. You have to spread those things a little bit apart.”

How do you make those decisions? What’s the line for you in terms of what you feel is reasonable to do for money as an artist?

“I think it’s a little bit easier for me, because I’ve not come from that world of commercial music, I’ve come from experimental, electronic music, club music, whatever you would say. It’s never been mainstream, so I’ve never been put in that position of saying, ‘Would you do this… to make money.’ I can’t remember too many instances in the past where I’ve gone, ‘I can’t do that, even if the money is really good.’ I’ve never really been put in such a compromising position. The offers for me tend to be more left field, whether it’s working for Manchester International Festival or BFI. I don’t feel I have had to make those ethical decisions.

“I love making music, but we’re not an elite, we’re not above, or better. Sometimes you have to work.”

“I’ve always tried to make sure that what I do connects with music, so even when I was writing or when I was running a radio station to make money, the core of what I was doing was still around music. I was happy to work around parts of music – I used to put massive gigs on in Australia, for thousands of people, which were really successful – but I still felt as though I was really connected with music.

“I guess you start to have this kind of portfolio career and I do kind of say yes to most things – and then regret it later! Not because I don’t think it’s been a good thing to do, but usually with me just because I think, ‘Why the fuck did you say you’d do that? I haven’t got any time to do it…’ It’s never an ethical or a financial thing, it’s usually a time thing with me. But I tend to get asked to do nice things, so I’m lucky.”

But the fact that you get offered that kind of work is, I would imagine, down to the decisions and the connections that you’ve made…

“I’m lucky, really, in the sense that I’m from a period where music and electronic music as we were making it in that early period was incredibly significant and held a much bigger role in people’s lives. There were less people making music, the impact was greater and it was getting into people’s homes because there was product in that way. I think what has changed is that with everything becoming digital and things going online, it has democratised it, so there’s just so much of it. I don’t believe it’s dumbed it down, I just believe it’s increased the amount of work that’s been produced and the difficult thing for people now is to just make themselves heard through the noise.

“You have to have your mind set to go, ‘I will never stop doing what is the core sense of myself’. But you also have to accept that It’s going to be a bumpy ride.”

“Also, music that 20/30 years ago was very core to people’s lives is just part of people’s lives is now – a smaller part of a bigger entertainment or digital creative economy. It’s a smaller slice of the cake now.”

So, knowing that, what would you recommend people do to sustain themselves while making music?

“I just think: ‘Don’t shut anything off.’ The next thing you do might not seem totally relevant to what your primary path is, like, I love making music and doing all those things, but I may end up doing something that is not literally based around me making a piece of music, but what it might lead to is something interesting. So, you know, I enjoy teaching in Sound Art and working with the people who run the programme. It’s nice to do that because it offers so many different things. You need to think much more broadly in terms of what you’re doing, nowadays.”

One of the big struggles is how variable people’s incomes are. Have you figured out anything that helps you deal with that?

“Quite honestly, not really! Sometimes you have to work – that’s the human condition. As much as I love making music, we’re not an elite, we’re not above, or better [than others]. Sometimes you have to do that. The only thing that is difficult and this is probably the nub of it, really: for a lot of artists and musicians they don’t really sit comfortably in those worlds. They make music because it’s an expression of who they are and sometimes that’s because not everybody sits easily in the outside world. I think that’s the difficult thing.”

So what has proved helpful for you in this process of adapting?

“Well, I did a degree when I was really young and was the first member of my family to do it, but it did kind of make me believe that I had other things to offer, I suppose. I think that’s the difficult thing. You have to sometimes go, ‘Well, I’m going to have to do this…’ You have to separate it. Like everybody else, I’ve adapted to the situation and thought, ‘Well I need to be doing other stuff.’

“You have to have your mind set to go, ‘I will never stop doing what is the core sense of myself’, whether it’s music or making films. But you also have to accept that it’s going to be a bumpy ride. I accept that there will be times when this is the primary part of my life and there may be times when I’m not flavour of the month and I’ve got to do other things.

“But I think people who really want to do these things, they’ll never stop. I think if you’re really into it, you never give up. You can’t. You just have to adapt. We’re humans, we have to adapt.”

Credit: Paul Burgess

How I Make It Work is a series of interviews with a variety of creative professionals, where we discuss personal experiences and lessons learned about money in the creative industries.

How can we help you?

What issues are you facing? What questions do you have about managing your money in the creative industries? What would be most helpful to you?

We don’t have all the answers, but maybe we can find someone that does.

Manchester’s mainstay DJ and new music obsessive Shell Zenner on how she makes, saves and tracks money from a diverse range of music gigs

Shell Zenner somehow blends together a career involving multiple radio shows, club nights, DJing and a huge variety of other activities, all of which revolve around an almost surreal level of dedication to new talent.

Having gone full-time in music a year or so back, she is in some ways the consummate modern media worker, pulling together a variety of incomes and a strong sense of her personal brand to sustain herself in the music and broadcast industries.

Unsurprisingly, keeping on top of her various work and projects requires a remarkable level of personal and financial organisation, so we couldn’t think of many people better placed to discuss the challenges, tips and tricks of money in the music and broadcast industries. Fortunately, Shell was generous enough to share her insights…

How would you describe your current role, given the many different strands to your work?

“I would describe myself as a ‘radio-presenter-producer-curator-music-journalist – that does digital’. Does that make sense!?”

Er, yes… How many different sources of income do you have?

“Well, I don’t do any free work unless it’s for charity, so everything else I do is paid. There are a couple of things which will pay me PAYE [Pay As You Earn – i.e. taxed at source], which is BBC work, whether freelance or staff, so I work a day and a half a week for the BBC. I do two days for my XS show, which is freelance, and my Amazing Radio show is freelance, then I do various other little projects…

“The more skills you’ve got, the stronger a position you’re going to be in”

“So things like DJing, which is obviously not happening at the moment, but I normally co-curate nights with [Manchester venue] Band On The Wall, I do lecturing, I do hosting, I’ll get paid for filmed interviews for brands, build playlists, write articles, host online gigs – and I also do voice-overs. And I’ve forgotten about artist development! I’ve been doing quite a lot of that over the last 12 months, which has been really great, being able to mentor new artists. I’ve also done things like assessing funding applications for PRS and Help Musicians. All of that ‘top-up’ work [outside of radio], is all freelance.”

There are so many poor unpaid ‘opportunities’ in the creative industries. How did you go about finding such a variety of paid work?

“I find it mostly comes to me now. I think that’s about networking and about being a sure thing and also having a big palette of skills. So, if someone wants a voice over, I can copy-write, I can voice it, I can edit it. It’s having a home studio and the equipment you need, it’s having contacts at facilities and a rapport with people.

“[In terms of networking], it’s just about talking to people because you’d be surprised – that conversation might not lead to something right now, but it could in six months time. If a project comes up, they may think of you. It’s also about wanting to keep learning new skills and pushing your knowledge because technology is changing all the time. Now I’m able to video edit and film myself and things like that make a big difference. Again, the more skills you’ve got, the stronger a position you’re going to be in.”

Want to make sure you never miss a post? Sign up to the Creative Money newsletter!

Do you think we have an issue with financial literacy in the creative world?

“Yeah, you’re absolutely right. I do a bit of lecturing and often wind up talking about how I budget or how I organise myself and I think it is illuminating for people. [It’s surprising], even freelancers at the BBC, where they get tax deducted at source, don’t know how to handle freelance earnings and DJ money and stuff like that. And people don’t know how much to charge for stuff, so it’s about having the balls to stand up and say how much you need to be paid. I’ve had to point out to people like, ‘That’s going to be paying me below minimum wage, once I take the tax money off.’ Once they think about it, they will up the money then, but you have to have the strength of character to do that as well, because there’s a risk you could lose the work.”

A major issue for many in the creative industries is the ups and downs of cash flow. How do you deal with that situation?

“There’s a couple of things that I think are really important. One is always having some savings. I grew up in another industry [engineering], and I never really wanted to depend on anyone else, so I always made sure I had a bit of money to cover one or two months, should anything go wrong. I worked this career up over 10 years – I didn’t take the plunge to go fully radio/music until last year. I’ve always been quite risk-averse but that has stood me in good stead because I built it up over such a long time and wore so many hats.

“The other thing is that I’ve been really clear about keeping spreadsheets for earnings, expenses and mileage and understanding what you can and can’t claim as a business expense. I got myself an accountant and you think, ‘Oh I don’t want to pay that kind of money’, but an accountant is a tax deductible expense and they don’t always cost the earth. Having someone there that you can run stuff by gives me the sense of security that I’ve done everything correctly and am not going to find myself in trouble and needing to pay a big sum of money down the line.”

How do you handle things like invoicing and tax savings?

“Every freelance earning you make, regardless of whether it’s paid in cash, you still have to invoice, so it’s having systems in place for invoicing and saving invoices. Then, for me, it’s making sure that whenever you get a payment you are – right at source, as soon as it comes in – taking 30% off for tax and national insurance and putting it in a separate savings account. I have two linked [savings] accounts at this point, one for the last financial year and one for the current one. I got my tax return back today and it says I’m getting a rebate! So not only do I not need to pay it, I get a rebate. Now I’ve got some extra money and I can think, ‘What can I invest that in?’ Or give myself more of a buffer.

“You hear people say, ‘Right, I need to go and sell my car so I can pay my tax bill.’ That’s insane!”

“I’m not the messiah of tax but I’ve seen friends fall foul of that who have worked in the creative industries, so I think it’s worth being super organised and giving yourself that buffer. If I have that money there, I also know that if something goes drastically wrong then I have that flexibility. You don’t want to be living hand-to-mouth if you lose one of your roles. Some people rely on one particular organisation for a lot of their work, that’s pretty normal for most people, but then if you do lose your role you’re in quite a catastrophic situation.”

Do you use any fancy financial software to help you keep track?

“There are people that track things in more modern ways, but a spreadsheet is fine for me, so I keep an eye on my income, my receipts, my mileage and just have it all listed in one document. If you can do that and update it week-by-week, it just makes your life so much easier. Then when you get to the end of the financial year, you can just have a quick check-through and send it to the accountant for the final number crunching. The amount of people you see who are at the end of December and January, trying to do their tax returns and panicking… I’ve seen that a lot. That thing like, ‘Right, I need to go and sell my car so I can pay my tax bill.’ I’m just like, ‘What!? That’s insane!’”

What are the financial issues or mistakes you think people should be wary of as they try to keep their head above water in the broadcast or music industry?

“I think if you are in a situation where you are pitching for something and you’ll need to hire a lot of equipment or pay out for locations then you’ll need to be really watertight on your contract. If you lose the job and you’re having to pay, then having policies in place for that kind of stuff is really important. Insurance, too. For instance, I have public liability insurance and I try to cover myself to make sure if I say anything on air [that could lead to a lawsuit]. You just have to protect yourself really well and prepare for every eventuality. I’ve done a lot on this, my career before this was engineering so I was into health and safety, risk assessments and stuff like that!

“The worst thing you can do, business-wise, is promise things and then not deliver”

“It’s also about always having a contingency [plan] so that should anything go wrong, you’re not out of pocket, because ultimately you need to be making profit. Even if it’s just a small profit. You may be gaining from a project in a different way, whether it’s experiences or contacts, so you may be willing to do something at a stripped-back rate to gain that network and that experience, but it’s still important to make sure you’re not going to end up out of pocket.”

Is there anything about money in the creative industries that you would like to change for the better?

“I would definitely like the BBC to change their freelance policy. I was angry about this before, but the lockdown situation has really brought to light the major issues with it, which is that if you work as a freelancer at the BBC, you get taxed at source and that means you can’t claim the mileage or any of the expenses [nor do you have the perks of full-time staff]. So should you need to travel two hours to get to a job, you can’t claim that mileage, you can’t claim any equipment you might need to do that job.

“[The BBC have stepped-up to offer furlough payments for freelancers now] but there were people who lost all their work because the BBC has changed schedules etc., which is fine, but if you go to HMRC and over 50% of your earnings are PAYE, then you are not eligible to claim on the Self-Employment Income Support Scheme. So that’s meant there were a lot of freelancers who couldn’t be furloughed because they weren’t technically ’employed’ by a company, they couldn’t claim for the self-employment benefit and all they had left is Universal Credit, which is very little. If you are paid as a freelance, you shouldn’t be taxed at source, you should be figuring out your tax through a tax return and you should be able to claim your expenses. I question why freelancing at the BBC has to be taxed at source, it just doesn’t seem consistent to me.”

“I’ve been trying to support [the #ExcludedUK campaign] on Twitter and stuff. These people have really fallen through the cracks and it’s just pretty insane really. It just blows my mind.”

What would you say to someone trying to figure out how to sustain themselves within the industry?

“Maybe just that it’s good to give yourself a financial buffer. It means you don’t have to flog yourself just to survive at times. The problem is in the creative industries is that self care is something that’s often overlooked. You feel like you need to be ‘on it’ 24/7 and sometimes, for whatever reason – you’re not very well, or you’ve got family issues – giving yourself a little bit of a buffer can enable you to take some time out and give yourself a breather. You can push yourself too far with the pressure of it, so having some savings there really helps.

“Also, it’s about not over-stretching yourself with work and trying to be realistic with what you can accommodate and do. The worst thing you can do, business-wise, is promise things and then not deliver.”

The summary:

Spread your risk. Zenner worked a day job for nearly a decade before taking the plunge full-time in music. She also now has a huge variety of income strands.

You need savings. Make the effort to syphon off tax money as soon as it lands in your account and build a savings buffer to get you through tougher times.

Network – and deliver! We don’t mean lunch at The Ivy. Just talk to people. You never know what might happen down the line. And, crucially, make sure you follow through on any promises you make.

Keep building your skillset. Zenner has consciously expanded her skillset to include writing, recording, editing and video, alongside promoting and industry knowledge. All of these can provide a source of income.

How I Make It Work is a series of interviews with a variety of creative professionals, where we discuss personal experiences and lessons learned about money in the creative industries.

How can we help you?

What issues are you facing? What questions do you have about managing your money in the creative industries? What would be most helpful to you?

We don’t have all the answers, but maybe we can find someone that does.

You know you should start saving but you don’t. Can we change that?

Everyone knows they should be saving, but while this painfully obvious advice is wheeled-out ad nauseam, the bigger issue is HOW to start saving in the face of personal limitations, whether they’re financial or mental. Here are five tips to help you get started…

Savings are a catch-22 situation for many creative workers – if your earnings are low or inconsistent, then it’s more important to have the security of savings, yet harder to build that cash cushion. It’s no wonder many of us feel it’s impossible to start, particularly amid the current economic situation.

If you’ve tried and failed to save before, or are looking for a way to start, consider instead how you can create a process – a savings production line for yourself.

Lofty and unsustainable savings goals can do more harm than good. Make it your aim to simply start

Lofty and unsustainable savings goals can do more harm than good for new savers, demotivating us before the habit is established, so try focussing on forming and rewarding the habit itself.

Make it your aim to simply start and set something aside for a period of time, if the amount varies or seems small that’s still a victory. You’re building a habit right now, not a war chest. Once the habit is formed, you can build from there by increasing amounts and starting to think more about where to direct the cash.

Whether’s it’s £1 or £100, most of us can save something – and something is always better than nothing.

Want to make sure you never miss a post? Sign up to the Creative Money newsletter!

If you have any form of regular income, whether it’s salary, recurring freelance work or even a benefit payment, set up a standing order to your savings account to go out the day it lands in your account. Start small. The aim is to set aside an amount that you won’t notice is missing later in the month.

If your income is entirely variable, create your own automation by setting aside a small percentage from each payment you receive – again, start small – try 5%.

2. Round-up your spending

There multiple banking apps out there now that will enable you to round-up transactions to the nearest pound and deposit the difference in a savings account. This can be useful for freelance and creative workers because it creates a form of automation that’s not dependent on having a predictable, consistent income.

If you have an issue with raiding your savings, then pay them into an account with a different bank or building society and don’t check the balance. Just pay it in regularly and forget about it. Consider this money dead to you for the year – a gift to your future self.

Your future self might want to check the balance in 12 months, or in the New Year, or tax season. But by that point the habit should be set.

Finally, make sure any institution that you save with is UK-regulated and therefore covered by the Financial Services Compensation Scheme (FSCS) – this protects your savings (up to £85,000) if the bank fails.

This is a great idea if you’re used to spending all of your income. Start by setting aside an amount you know you won’t miss and then increase the standing order every month. It allows your spending to adapt slowly and in a way you will scarcely notice. Even if you start with £5 and increase £5 a month from there, after a year you could wind-up with £390 in the bank and a regular savings habit of £60 a month. At that point, even if you don’t increase the standing order any further, you would be setup to save a further £720 in the following year.

5. Get the government to help you

If you’re entitled to Working Tax Credits or Universal Credit, you may be eligible for a Help To Save account. If accepted, you can pay in between £1 and £50 a month and the government will give you a bonus 50p for every £1 you save.

The bonus is paid after years two and four and is based on the highest balance you managed to save in each two year period. If you pay in the maximum amount each month, you could save £2,400 over four years – and get an extra £1,200 from the government. That’s a guaranteed return of 50% on offer, which is huge!

Here you’ll find a list of UK arts funding opportunities, split into sectors. Also included are other grants and selected development or training opportunities relevant to the creative industries.

Current opportunities will usually appear first in the Creative Money newsletter and then filter through to this page. The newsletter is totally free, so sign-up below if you want to get a head start.

Want to make sure you never miss a post? Sign up to the Creative Money newsletter!

Want to let an audience of UK creative workers know about a funding, grant or development opportunity? Seen something we’ve missed? Drop us a line using creativemoneycontact@gmail.com.

Supports artists, community and cultural organisations with grants in the range of £1,000-£100,000. Their remit has been tweaked (and will remain so until April 2021) for the recent relaunch in order to better respond to the needs of individuals, freelancers and small organisations working within or supporting the arts.

Funds UK arts/social charities (particularly performing arts) on an ongoing basis with grants ranging from £10,000 up to £1 million. You can apply anytime but it’s worth noting that the trustees only meet to make decisions twice a year – normally in June and December.

Funds registered UK charities working within the arts sector – in particular, projects relating to the nurturing of talent and development of professional opportunities – with grants of up to £5,000.

All or part of the project must be presented in Australia between 1 September 2021 to 13 March 2022 and align with the theme ‘Who are we now?’ Deadline: 17 August, 2020

Work/Leisure is inviting emerging and mid-career artists, living and working in the UK/Europe, to create new work in 2020. Successful applicants will be provided with an overall budget of £1500 and administrative and curatorial support from the W/L team, Abingdon Studios, and residency partners. Deadline: 17 August, 2020

Jerwood Art Fund Makers Open 2021 has five £5,000 grants for early-career UK-based artists and makers to develop and present ambitious new works. Deadline: 26 August, 2020.

Unlimited is an arts commissioning programme that enables new work by disabled artists to reach UK and international audiences. They will have £500,000 to commission work from disabled artists and companies in three strands: Main Commission awards, Research and Development awards and Emerging Artists awards. Applications don’t open until October, but they’re getting the word out nice and early. Deadline: 27 October, 2020

A fund to support emerging UK creatives in all-forms of non-fiction film, including immersive and VR projects. Successful applicants will get a grant of up to £15,000 for production costs and projects must not be more than 40 minutes in length. Deadline: 18 August, 2020

The Commission is launching a €1.5M call for proposals to create innovative cultural hubs around cinema theatres, notably in areas where the Covid-19 crisis has had a very strong impact. Deadline: 21 August, 2020

Creative England’s New Ideas Fund can offer grants between £1000 and £25,000 to support the development of new and innovative ideas for screen-based storytelling entrepreneurs and businesses in the English regions. Applications considered on a rolling basis.

A development and networking platform from the BFI, aimed at supporting new and emerging film talent. Offers some funding, though its short film grants have been currently paused due to COVID-19.

Intends to back projects that might not otherwise secure early-stage financing, though you need to demonstrate prior filmmaking experience to qualify. Funds have been tweaked to front-load payments, if necessary, during COVID-19.

Yes, the name is daft, but this is an incredibly helpful tool for quickly assessing your music funding options. You simply enter some information in the form (type of musician, genre, career stage etc.) and it produces a list of potential funding opportunities for you.

Publishing

Call for disabled writers to pitch arts pieces

Art UK is looking for pitches from disabled writers who want to write about art and artists. Explore http://artuk.org for inspiration. Rates are around £100–£150 for pieces between 700 and 1,200 words. Send your pitches to andrew.shore@artuk.org and lydia.figes@artuk.org

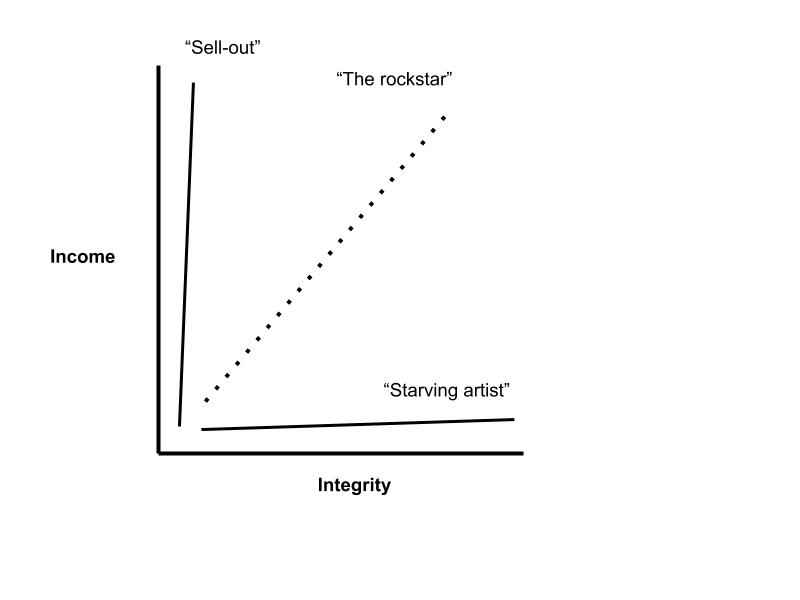

Our thoughts on the financial outcomes of life as creative workers often seem to fall into two categories: ‘the starving artist’ and ‘the sell-out’. If only it were that simple…

I would wager that everyone who earns money from creative work has wondered at some point whether or not they’re ‘selling-out’. The tropes at the heart of this struggle are are within us all: the starving artist has unimpeachable integrity but negligible income, while the sell-out picks their gigs by the paycheque. They remain locked in combat, fighting for our very souls.

We’ve all likely had cause at some point to embrace the starving artist and some of us even come to experience life at sell-out end of the scale – gaining a full understanding of the ambiguous privilege of considerable wealth and fame.

Straight line thinking – how people often think about income and integrity

Sometimes, we may also consider the evener rarer ‘third way’, wild success on our own terms – let’s call this ‘the rockstar’ – but this often seems even further removed from our view of the achievable (though Seth Godin’s The Icarus Deception argues the opposite).

At other points, we may feel we have no option but to leave an industry, or take some other work on in purely to pay some bills.

Anyone who’s even come near to experiencing true poverty knows that the starving artist cliché is a false romance

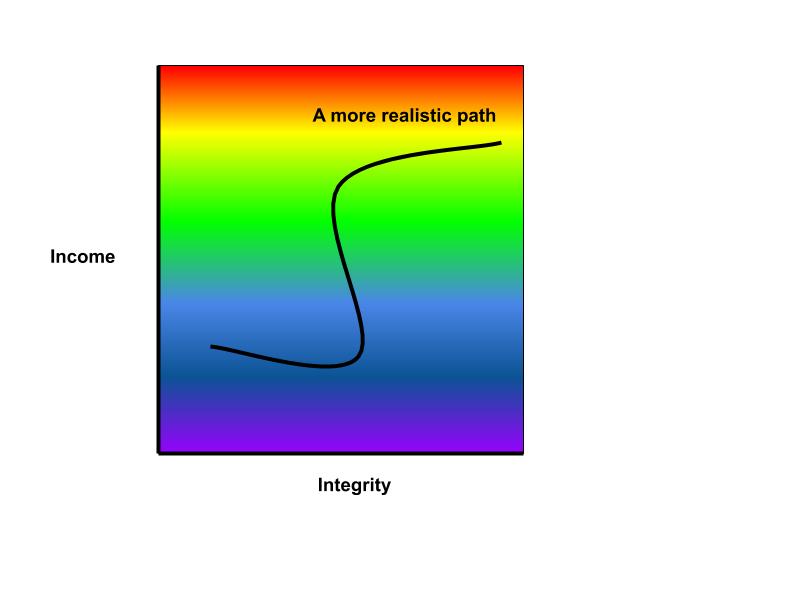

What’s interesting is the extremities of these viewpoints – that we seem to ascribe the myriad outcomes of our creative work as an ‘all or nothing’ endeavour. The truth of it, though, is that it is a spectrum – and that existing on that spectrum, rather than at one of two extreme poles, is not such a bad place to be.

Anyone who’s even come near to experiencing true poverty knows that the starving artist cliché is a false romance. It’s been perpetuated throughout history, often by patrons in positions of wealth, but while understanding or experiencing poverty and the broader human condition has no doubt informed great creative work, it is certainly not a route to happiness. In fact it is, by definition, a direct route to unhappiness.

What’s it worth?

At the other end of the scale, it is widely acknowledged that while wealth can help you ‘buy’ a certain level of happiness, the benefit of greater wealth tails-off dramatically once you’ve covered your basic needs and a few extra comforts. This is a phenomenon that US blogger Mr Money Mustache has popularised and termed the Marginal Utility of Money.

Want to make sure you never miss a post? Sign up to the Creative Money newsletter!

Even Warren Buffett, the 89 year-old billionaire CEO of Berkshire Hathaway – and at one point the world’s richest person – counsels against the pursuit of wealth for its own sake. And this is a guy who bought his first shares aged 11.

“Doing reasonably well in this country really is pretty darn good,” he said, talking to US students in 1999. “Great wealth is the tiniest bit different, in a real sense, than having just a decent income. To trade a decent income and something you love doing… for huge wealth where you trade a lot of your principles would be a terrible mistake.”

So, if we agree that both extremes are flawed and stop trying to define our financial personalities against a minority of outliers, what does the right path actually look like? And what’s a reasonable income?

Great wealth is the tiniest bit different, in a real sense, than having just a decent income

Warren Buffett

That is yours to decide. For me, it’s enough to cover living expenses, to be able to pay for a few home comforts and holidays and to save enough to retire within the next 25 years (WHAT!?) At the more luxurious end, I’d like to spend as little time on compulsory work as possible. I like my work, but I value freedom even more.

Figuring out the numbers behind these goals is really useful to making sure you’re actually on course to meet them.

I discussed why tracking your spending is key to understanding your cash flow (and therefore getting some control over a variable income) last week, but there are other benefits to that process, too. When you know how much you spend, you know how much is enough. You know when you can stop, or say no.

As far as possible, I’d also like to get to these points above without doing work that I do not personally believe in.

“‘At the end of the day, you only have yourself to answer to.’ Regardless of having to pay your bills, keep to deadlines… if it ‘sits right’ – then that’s okay.’”

If you operate with integrity, then you avoid selling-out yourself, but only you can judge what that might look like.

The ‘starving artist’ trope comes from a belief system and, as with any belief system, there will always be a vocal minority of hardliners, who refuse to question the dogma out of some fear that the world will unravel. Instead, each of us needs to decide on our personal beliefs and principles around money and creativity – and make decisions accordingly.

There’s a broad, rich spectrum between ‘the starving artist’ and ‘the sell-out’

If you lean towards the starving artist axis then, contrary to the thinking of many, you’ll likely need to watch your expenses closely. What’s more, planning for the future and times of poor cash flow becomes even more essential.

If you lean the other way, gaining a higher income, then you may have more flexibility with your spending and insurance against the risks you take (some of which might pay-off handsomely). However, to gain true satisfaction from your work, you will likely still need some measure of your personal values built-in to it – lines you don’t cross. This might be to do with the ethics of the organisations you work with, the relative creative appeal of jobs etc. Knowing your values helps you to navigate the path.

The full spectrum – the options are much broader than many of us realise and the path you tread might change according to your priorities at the time

For instance, in my case, I am open to many different types of work. My main gig is music journalism, but I’ve written copy and advertorials, I’ve run events and managed projects, I’ve led degree courses and taught. But I’ve come to understand that if the only reason I want to take a job is the money – and I can find no other appealing features in terms of the work, my personal or career development, or the organisation I’m working with – then I am going to regret that decision.

Not everyone will feel that way – or feel they have the option to do so (particularly right now) – but that’s OK. Indeed, that’s the whole point. Creative Money is not here to promote the pursuit of untold riches, but simply to help you figure out how you can sustain yourself over the long term as a happy, creative person.

There’s a broad, rich spectrum between the tired clichés of the starving artist and the sell-out. Where do you want to be?

We talk useful financial/career resources for journalists, industry barriers and the difficulties of managing money as a freelancer

For this week’s How I Make It Work, Creative Money spoke to Lydia Wilkins. A freelance journalist, Wilkins [pictured above, right] has had bylines at a string of significant publications, including The Independent, The Metro and Readers Digest. Wilkins also writes her own blog, Mademoiselle Women (in which she documents life on the Autistic spectrum) and pens an excellent weekly newsletter. She is currently busy developing these into sources of income.

Like many of us, Wilkins is in the process of attempting to weave these various creative threads together in order to form a viable freelance career and support herself through her writing.

We spoke via email about the resources that have helped her figure it out thus far, what she’d change about the treatment of freelancers and how she goes about keeping track of her finances, despite her struggles with numbers.

How would you describe your current role?

“I’m a multi-hyphenate freelancer! I blog three times a week at mademoisellewomen.com. I contribute regular freelance articles to places like The Independent, Readers Digest, Refinery 29 and The Overtake – usually to do with travel, book, or autism. I’m also a webinar trainer for a small organisation that teaches strategies about Autism. I also run a weekly newsletter; this has interviews, a comic I’ve been able to commission, as well as resources for freelancers and Autistic individuals.”

“It’s insulting to ask me to do whatever for ‘exposure’. Exposure isn’t a tangible concept – it doesn’t pay my bills”

Do you ever do unpaid work? What are your thoughts on this?

“Very, very occasionally. Right now, the blog is not profitable – despite ‘breaking even’ last year – due to the pandemic. Sometimes smaller magazines that cannot afford to pay allow you to pursue a story you wouldn’t have been able to take up elsewhere. I recently interviewed Lissie for BN1 Magazine – everywhere I pitched had quite specific rejections, she did not ostensibly fit the ‘brand’, etc. I got to interview her down the phone – and it’s still one of my favourite interviews I’ve conducted.

“That being said, I don’t think it should be allowed. Freelancers are highly qualified individuals. They are just as valuable as staff reporters – you should be paying for the service you use. I sometimes feel like freelance contracts have just been used to pay less, to still create a quality product – but we need time and resources… it’s insulting to ask me to do whatever for “exposure”. Exposure isn’t a tangible concept – it doesn’t pay my bills – so why would I agree to that?”

Want to make sure you never miss a post? Sign up to the Creative Money newsletter!

What decisions or experiences have proved most valuable in helping you to establish yourself within the industry?

“Firstly, I have been invited to events that Hacked Off have held. While the issue of press regulation is still controversial, it was utterly harrowing to hear the stories of people who’d been harassed, placed under surveillance, etc. Journalism has a responsibility; we are the gate-keepers, but we cannot behave in such a way to people, regardless of fame or fortune. I have this at the forefront of my mind most days – and it informs the way I talk to sources.

“Secondly, ‘If you don’t ask, you don’t get’ is a phrase I grew up with. Derren Brown wrote of changing our stories, the stories we tell ourselves [essentially, making the choice to reframe the way we view ourselves and our limitations] – and doing that can work really well.”

What have you found to be the best resources in terms of figuring out how to earn money and sustain yourself as a journalist?

“Journo Resources was the first website I came across, while studying, that I thought ‘they get it’. As an Autistic individual, I have often had to battle to be heard – and not just be taken as someone who ‘suffers’. (Yep, this has been said to me on several occasions – and is a disgusting trope. It also can prevent me doing the job I do.) There is a wealth of resources, and I learnt a lot more than I thought I would – with CVs, how to invoice, and more.

“The Bloglancer is run by journalist Jenna Farmer. It’s a blog about how to make money blogging, as well as freelance journalism. Here was someone experiencing the same I was – who was maybe just that little bit older, and a little bit wiser! The posts are accessible, cover a slew of issues, and I have gotten some work from the fortnightly jobs board.

“PressPad is an organisation that is devoted to #DiversifyTheMedia. I wish they’d been around when I was starting to get interested in journalism! The pandemic means they’re running a great outreach programme – with masterclasses, CV clinics, and more.”

Lydia Wilkins (right)

Have you had any good financial role models?

“Not really, no…”

How do you attempt to deal with the inevitable ups and downs in cash flow that come with freelancing?

“I must admit, I am not really sure how to answer this one…”

Do you find that you have to keep a close eye on your finances? What tools and resources help you to do so?

“Yes. My support worker has suggested I may have a condition that affects my ability to interpret numbers – it’s something I really struggle with. I use a form of journaling, month by month, to keep a track of my finances – such as with ongoing invoices, and keeping a visual record of my financial history. Bullet journaling can help.”

Are you saving for retirement? Is this something you feel is feasible?

“Not just yet! I am looking to get into full-time employment. Though I am a trained reporter – and have interviewed people like Anastacia, Sir Harold Evans, Jodi Picoult – I have often found myself on the end of discrimination. I am slowly transitioning; then I will save for retirement.”

“I use a form of journaling, month by month, to keep track of my finances”

Is there anything that bugs you about the way the industry operates, particularly in terms of finances or money management, that you would like to change for the better?

“What bothers me is the way freelancers are treated. You are supposed to be paid within 30 days – and late payments can apply. This is the law, yet so many publications willingly flout this! Apparently, it takes 45 days to get set up on one finance system, I was told for one publication. And I think I also had to follow up that payment… Freelancers are becoming more and more used, across more and more industries. It’s about time they were treated fairly – with pay that’s in line with a staff job, equal across all characteristics – and not just as an afterthought.”

Have you noticed any issues relating to finance that might prove a barrier to diversity in the industry? And do you have any ideas for improving the situation?

“I’m not sure I have any practical solutions. It’s a really good question to be asking, but it is not always to do with hiring, but more about [what we can do] at an educational level. For journalism, if your parents are university educated and were reporters – plus, being male and white with your own degree – it gives you a hell of an advantage… I wouldn’t know what to say to that – but I wrote about it here.”

What’s the most valuable advice you can offer to someone starting out in the industry?

“One of my mentors worked for Reuters, and is sometimes looked-up to as a kind of ethics authority. I asked for him, and I remember the most valuable piece of advice he gave me: ‘at the end of the day, you only have yourself to answer to.’ Regardless of having to pay your bills, keep to deadlines, as long as you are okay with what you’re doing – if it ‘sits right’ – then that’s okay.’”

The summary:

If you’re going to write for free, write for yourself. The much-vaunted ‘exposure’ offered by non-paying platforms is rarely worth it. Spend the time building your own audience.

Change the stories you tell yourself. Do you avoid pitching opportunities for fear of rejection? This can be a self-perpetuating cycle: fearing failure means we don’t try, which results in guaranteed failure. Instead, try telling yourself ‘I need to give it a go to find out if this works…’

Find resources that demystify your industry. There are some excellent resources emerging for the world of freelance journalism and writing. Check out Journo Resources, Press Pad and The Bloglancer.

Try bullet journaling to get a visual representation of what’s happening with your finances, month-to-month. If you struggle with numbers, bullet journaling can give you a more ‘hands-on’ sense of your cash flow. Here are some ideas on that.

Journalism is still dominated by white males with degrees. Diversifying access to education and training is key to addressing this imbalance.

How I Make It Work is a series of interviews with a variety of creative professionals, where we discuss personal experiences and lessons learned about money in the creative industries.

Are you self-employed, freelance, or a contractor with a variable income? Here’s how to cope with the financial peaks and troughs

Nearly half of creative workers (47%) are freelance or self-employed (source: ONS, 2017). Chief among those are writers, producers, artists and directors – it’s a large and significant part of almost all creative industries. One of the key challenges for this group is managing money on an irregular or variable income. So what can we do to smooth-out the financial ups and downs that we will inevitably face in a given year?

The key is learning to syphon-off your income in normal and higher-earning months into a ‘top-up fund’, so you can top things up from your savings when needed.

This would be easy if humans were calm, logical creatures, but we’re not – so we need a way to tell whether or not we should save or withdraw (and by how much) in a given month.

Turning a problem into a question

If we put a little effort in upfront, we can save ourselves from guesswork down the line.

In order to do this, we’re going to answer these five questions…

Why? Well, if you know how much you earn and how much you spend in a given month, you can figure out what you are left with. This is your personal cash flow.

All businesses ultimately survive or perish based on their cash flow (overall, is there more money flowing in than flowing out?) and it’s the same in your personal finances.

Once you have a predicted cash flow figure for the month, you know whether you will likely need to pay in or out from your savings (your ‘top-up fund’) for that period. This will help smooth-out that variable income over the longer term.

Answering the final question (‘How much do I need?’), gives you the comfort of knowing the minimum amount you’ll need to live on in a given month. The bigger the gap you can create between your income and this essential spending, the more you can potentially save into your top-up fund – and the bigger cushion you’ll have to smooth-out the financial ups and downs.

This is quite a lot of information to pull together initially, so I’ve put together a spreadsheet to help you keep track and – if it all goes to plan – to do some of the calculations for you.

Free spreadsheet!

The sheet is designed to be used to log your answers to some of these questions and calculate your cash flow for a typical month.

You can then stop there, or you can use it to keep track over the longer term. Keep it up-to-date and the sheet will help you figure out how to spread your variable income more evenly throughout the year. We do this using a ‘top-up fund’.

You can download the sheet above and there are links and tips (in bold, with the lightbulb icon) throughout this piece to help you understand where to enter the relevant information.

Even with the whizzy spreadsheet above, this stuff can take time, so don’t stress if you find you have to do it in instalments. The clarity is worth the effort.

1. How much do I earn?

First, let’s figure out what you have coming in normally.

If you have any salaried work (or state benefit) that pays a regular, fixed amount, use your bank statements or pay cheque to find out your monthly income.

Make a note, or add this into the top ‘Salary income’ box for your ‘Typical Month’ on the supplied spreadsheet.

But I’m freelance and my income is a nightmare…

It’s a bit messy, but finding a past average is probably the simplest and most helpful place to start. We’re looking to smooth-out future dips and bumps in income, so a figure that represents the middle of your ‘normal’ range is useful here.

Ideally, you want to represent a long period with the average – a year or more – but you can hone this and update down-the-line. Right now, settle for making a start.

So… add up your income for your chosen period and divide the figure by the amount of months it covers.

Total income for period ÷ Number of months in period = Average monthly income

For instance, if you earned £12,000 in freelance income over 12 months, your average would be £1,000 a month.

Some ideas about where to find this information:

Banking apps (you may be able to just filter income only transactions)

Your income statement (where you track invoices etc.)

Your tax returns (dig out that Self Assessment login)

Ask your accountant

If you’re setup as a company, make sure you factor in your dividend income for the year here, too.

Once you’ve found it, make a note.

You can drop your average freelance income figure in the ‘Freelance income’ box of your ‘Typical Month’ on the spreadsheet. This will then be added to any salaried income or benefits you specified, in order to tell you your average total income.

Then take a break…

Want to make sure you never miss a post? Sign up to the Creative Money newsletter!

Now let’s figure out your spending for a typical month.

Sit down with your banking app or statements and go through your spending for the last month (or one you feel is truly representative of your typical expenses – if in doubt, be pessimistic).

Split the month’s spending into categories of fixed and variable expenses.

Fixed expenses

Your fixed expenses will be recurring bills and spending (e.g. rent or mortgage, insurance, gas/electric and other direct debits), which do not usually vary month-to-month.

Variable expenses are things that may might vary month-to-month, for instance: travel costs, food shopping, eating out, or gifts and entertainment.

It’s a good idea to make groups under your variable expenses to reflect your spending priorities and help you to see where your money is going. There are some examples on the sheet above already. Keep it simple, though – no more than 10 groups.

If you just can’t face doing all of this immediately, settle for totting up any expenses not covered in your fixed category and lump them all in one ‘other expenses’ group.

(This sort of thing makes accountants reach for the smelling salts, but you can always come back and split this out out at a later date.)

Yes! Or at least, sort of… There are several apps out there that will help to automate the process of grouping expenses. Some of the fancier bank apps do this and there’s also the likes of MoneyHub and Money Dashboard, which allow you to connect and monitor multiple accounts/banks.

You can set your own groups or categories for expenses, but you will have to check-in and tag/correct your transactions. However, it does ‘gameify’ it somewhat, so if you’re a phone addict, it could work for you.

Adding it up

Now add the total of your fixed expenses and variable expenses together. Hello, monthly spending!

3. How much am I normally left with (i.e. what’s my typical cash flow)?

If you’ve been using the sheet, just scroll down and look at the ‘cash flow for the month’ total to see what’s left in a typical month.

If you don’t want to use the sheet, you’re simply doing the following calculation for your example month:

Total income for month – total spending for month = cash flow for month

What does this mean?

If you have a positive number, this is an amount you can save to supplement leaner months, using a ‘top-up fund’.

Bear in mind, too, that this ‘Typical Month’ cash flow figure might look small, but you are using an averaged income at this point, so even a small surplus is a good thing. It suggests an overall trend of more cash flowing in than flowing out.

If you get a negative number at this point, it means that on average you are likely spending more than you earn (a negative cash flow), or are on course to do so in the near future.

Don’t panic – this is good information to have, but you will need to cut expenses or raise your income to sustain yourself over the longer term. Figuring out your essential expenses (Q5. ‘How much do I need?’) will help here.

4. How can I create a more consistent income?

The answer is to create your own overdraft, using a ‘top-up fund’.

As soon as you are earning more than you spend, set-up an easy-access savings account to set this remaining cash aside. This is your ‘top-up fund’. So how do we do use it?

One method is to simply use your average income (as logged under your ‘Typical Month’) as a guide, as follows:

Earn more than your average income?

Pay the difference into the top-up fund.

Earn less than your average income?

Withdraw the difference from your top-up fund.

Of course expenses vary as much as income and most of us will need to keep a closer eye on things.

If you want to keep a better track on your finances and expenses, update the sheet monthly with your income and predicted spending and it will tell you whether to save or withdraw the ‘cash flow for the month’ figure.

* Updating requires much less effort than finding the initial figures, particularly if you set up your expense groups using an app – you’ve done the hard work already.

My mind won’t let me do this. It needs shiny things.

I hear you. Some things that might help you:

Make the ‘top-up fund’ deposit/withdrawal early – as soon as you can once payments have cleared.

Keep your ‘top-up fund’ with a different bank. You still want easy access, but for some reason the mental difference of having to login to a different platform can make you less inclined to dip-in to those savings.

Use separate accounts for bills (fixed expenses) and variable spending. Direct your earnings to a bills account and then transfer a regular amount (your variable expense total) over to your spending account and spend according to your priorities that month, knowing your bills are covered. Once you run out of cash in your spending account, that’s your lot for the month.

Don’t think of your ‘top-up fund’ as spare money. It is essentially your future income. ‘Borrowing’ too much from it now is like a salaried worker asking for an advance.

5. How much do I need?

Need to create a bigger gap between your earnings and spending? First, find out your essential expenses…

Look over your spreadsheet/notes/crumpled napkin with your expense totals and consider which items could be cancelled or easily and quickly reduced, if necessary.

For instance, rent is still considered compulsory by most landlords, but you may be able to avoid the posh shops for a bit and spend less on food.

Add it all up. Now you know your essential spending – the bare minimum amount you could exist on from either your income, or savings.

Are you asking me to remove all joy from my life?

No, but this figure is really useful to bear in mind for a number of reasons, for instance…

If you’re making an effort to boost your ‘top-up fund’ or other savings (because income – essential expenses = your maximum current saving rate).

If you want a minimum earnings goal, particularly if you are risk averse and keen to always avoid spending more than you earn (creating negative cash flow) within a month.

If you’re assessing whether or not you can afford to pass on that boring work you’ve been offered, or start that new thing.

Keeping one eye on your cash flow is key to avoiding nasty surprises. If you keep the sheet up-to-date, it can help you do this.

It has columns for ‘Year Total’ and ‘Year Average’, too, which can be really helpful in showing whether your overall cash flow is positive or negative for the year, as well as your average income etc. The year average can then me imported to the next year to form the basis of your ‘typical month’ column and the cycle starts over.

As you get more confident, it’s a good idea to start to increase your top-up fund savings (by cutting costs, or boosting income) until you have at least a month’s ‘salary’ on-hand.

A final note…

This approach should be regarded as a useful rule-of-thumb. It is a collection of various techniques that have worked for me, but it is not 100% foolproof.

For instance, it initially relies on your past income and predicted spending trends prevailing to keep your top-up fund savings balanced, which (particularly in the current climate) will not always prove to be the case.

In addition, the more dramatically your income fluctuates (say, you have three or four ‘big’ paydays, which sustain you through the year), the more you will need to set aside before you start using this technique regularly. In this case, build the ‘top-up fund’ as much as you can for time being and implement the system following your next big payday.

Nonetheless, the above represents my best effort to date. As we gather more ideas and resources on Creative Money, I will endeavour to update this guide and the spreadsheet.

Ultimately, the minimum you’ll get out of it is a better knowledge of your earnings, spending and the importance of cash flow, all of which can be really useful. Give it a go and let me know how you get on!

How stereotypes prevent us from sorting out our finances

Creative and financial ability need not be mutually exclusive. The pervasive idea that if you are creative, you are bad with money, yet those with the artistic sentiment of a doorstop naturally have a handle on their finances, is a harmful cliche.

I saw the above quote referenced in MoneyWeek the other day and, while amusing, it also struck me as a perfect encapsulation of the creative industries’ self-defeating mindset around money. We’ve all been guilty of it at some point, myself included. ‘I’ve never been good with numbers, I just draw pictures…’ ‘Pension? I can’t afford dinner…’ etc.

‘Natural talent’ is just a starting point – it is how we develop our craft that really helps us succeed. The same is true of our financial ability

We love the idea of ‘natural ability’ defining the destinies of the great and good. It allows us to buy-in to a bit of real life magic and marvel at humanity’s shared prowess. However, it also offers us a handy excuse for our own shortcomings – a get-out clause that says, ‘If we’re not born with it, we can’t do it… So I won’t try.’

My experiences in interviewing musicians and other creative types for the last 15 years have taught me that whenever we discuss ‘natural ability’ there’s a bigger picture being missed.

Take two famous examples of ‘natural talent’: Daniel Day Lewis and Jimi Hendrix.

Day Lewis made his big screen debut aged 14 in Sunday Bloody Sunday, which is undeniably impressive. However, he spent another 13 years studying and developing his craft on theatre stages before he landed his first major film role.

Hendrix? Hendrix really was an amazing guitarist, but he practised so much he wore his guitar while cooking. And on the toilet.

Whether we’re talking theatre or fashion design, ‘natural talent’ is just a starting point – it is how we develop our craft that really helps us succeed. The same is true of our financial ability. You are not inherently ‘bad with money’.

Instead, we should consider both our creative and financial abilities as different but complementary skills – both building blocks for the attainment of lasting happiness. In that sense, the most important question to answer is, ‘How can we sustain our ability to do the things we love?’

If you are making your way in these industries, you very likely already have the creativity and the drive required to figure this stuff out

In trying to solve this problem, learning to handle our finances can really help. The good news is that if you are making your way in these industries, you very likely already have the creativity and the drive required to figure this stuff out.

That might involve honing what you do to the point where you earn more money doing it; figuring out how to syphon off income when you have it, ready for the times when you don’t; or making a smart move to a more affordable location. The more you start to think about it, the more solutions you will find.

Everyone can do something to get nearer to their, er, happy place. And you’re not alone, either. The more ideas, options and resources we share here, the easier that process is going to get, so if you have questions or suggestions, don’t hesitate to get in touch. I don’t have all the answers, but we have a better chance of finding them as a community.

Most importantly, though, do not let yourself fall in to the belief that because your work is creative, you are destined to be bad with money, or that it is hopeless to try. If anything the reverse is true, you’re likely already better with it than most of your peers, because you often have to manage on less – and you’re certainly better equipped to work around your limitations.

If you can come up with ideas for your creative work – be it scriptwriting, or sculpture – why not redirect just a little of that energy to thinking creatively about how you could make this thing last? Can you be creative with money?

Rich Robinson, the songwriter behind the Black Crowes and Magpie Salute, offers his thoughts on the line between creativity and commerce

“When you get signed, you have to quickly make a decision: do you want to be an artist or an entertainer?

“Bankers have taken over the music industry. They’ve done it for the last 25 years. These people have zero talent, but they’re the ones telling artists how to make records that sell. That’s all it comes down to, you know? ‘I can make you a lot of money if you do these things: dumb your music down, shorten it…’

Focussing on making money like that turns it into a service industry. It’s like, ‘How do you want your hamburger?’ ‘How do you want your coffee?’

“There has to be a broader scope in creation. And that goes for architecture, film, music, literature. Any kind of creative endeavour.”

“Instead of the creative element, we have to ask, ‘What’s it for?’ Is it for the sale of a toaster oven? Or is it a little more important than that? I see that it needs to be more important than that. It’s art and creation where people can actually have a friend. A song that you connect with can bring you solace and peace and validation. That’s the ceiling. That’s what everyone wants. That’s what we’re looking for.

“There has to be a broader scope in creation. And that goes for architecture, film, music, literature. Any kind of creative endeavour. What’s it going to leave behind? Is it something that future generations maybe could benefit from? Instead of just cynically writing these bullshit pop hits that no one will fucking care about in 10 years because they’re not saying anything.

“To me, a song like ‘It’s Alright, Ma. I’m Only Bleeding’, which is a Bob Dylan song, is more relevant now than it’s ever been. Look at a Bob Marley song and what he went through in his life and how those songs resonate stronger now than they ever did – and that’s what I’m talking about. That to me is what’s the most important.”

As told to Matt Parker in June 2018.

Rich Robinson, pictured left. Credit: Josh Cheuse

Short Cuts is Creative Money’s series of quick tips, tricks and thoughts about saving or making money in the creative industries.